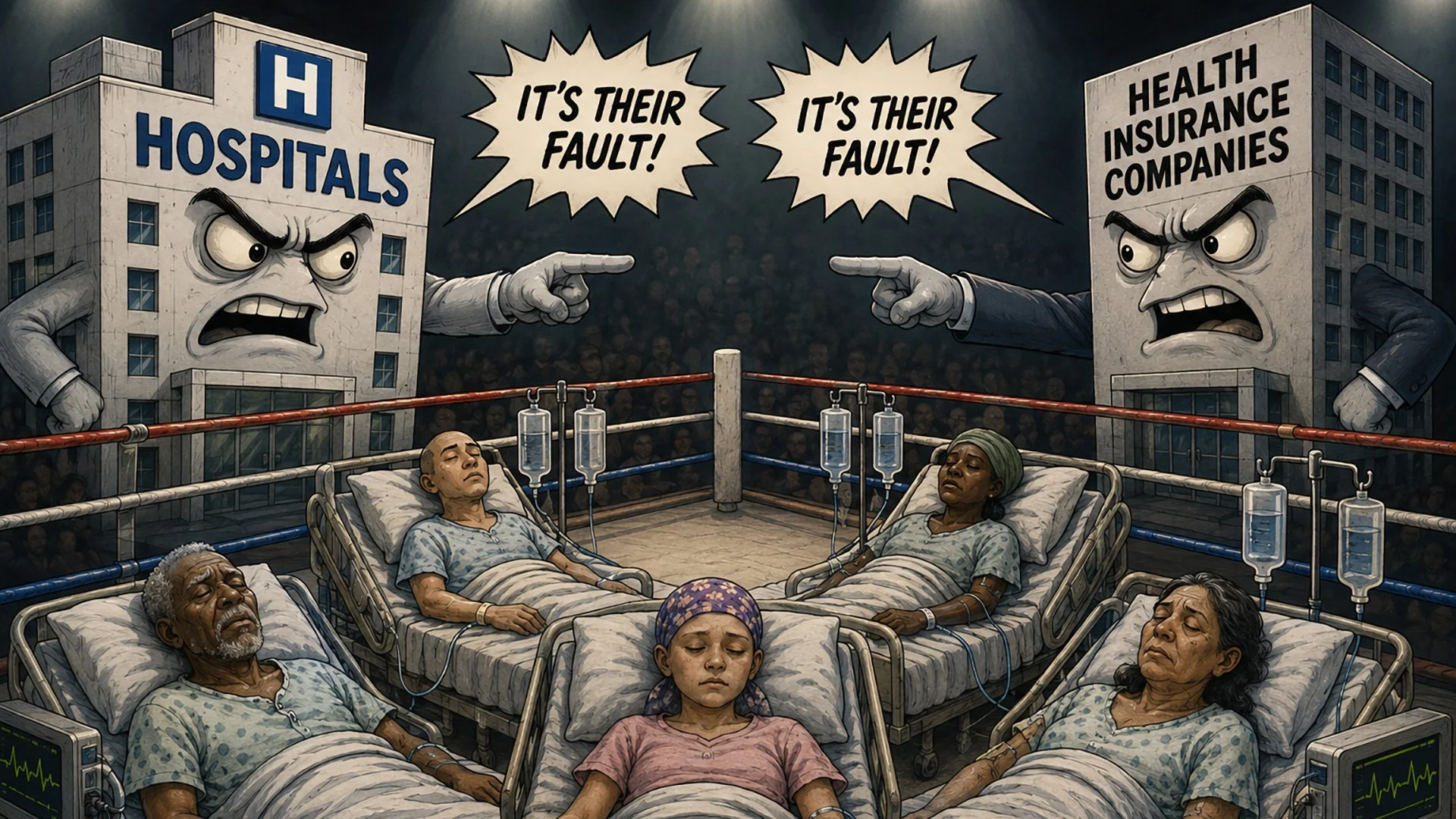

Hospitals and Insurers Keep Blaming Each Other While Patients Finance the Entire System

American healthcare keeps replaying the same argument because the argument itself protects the market structure. Hospitals blame insurers for denying care. Insurers blame hospitals for inflating prices. Policymakers choose whichever villain best fits their ideology. Patients sit in the middle financing the entire spectacle through premiums, deductibles, taxes, wage suppression, and personal bankruptcy. The conflict feels adversarial on television and in congressional hearings, but economically it functions as a deeply interdependent relationship where both sides benefit from complexity, opacity, and fragmentation.

That reality came back into focus after healthcare economist Zack Cooper published a New York Times opinion piece arguing that hospitals, particularly consolidated nonprofit systems, now represent the primary driver of healthcare inflation in the United States. Cooper pointed to a familiar pattern supported by years of market data. Hospital mergers reduced competition across regional markets. Dominant systems gained leverage over employers and insurers. Prices climbed dramatically even as quality metrics and patient outcomes showed inconsistent improvement. According to Cooper, insurers cannot effectively resist those price increases, so they transfer the pressure downstream through narrower networks, prior authorization requirements, denials, and higher patient cost sharing.

His argument holds substantial weight because the numbers support it. Hospital consolidation changed the negotiating balance of power across American healthcare. In many metropolitan regions, 1 or 2 systems control enough market share to dictate reimbursement rates. Employers and insurers often lack meaningful alternatives. A hospital system that owns the dominant trauma center, cancer center, physician network, and surgical infrastructure in a region can command pricing power that resembles a utility monopoly while still operating inside a nominally competitive market.

Then Wendell Potter responded with a critique rooted in institutional memory. Potter argued that insurers have spent decades cultivating precisely this narrative because it redirects public anger away from insurance industry conduct. He knows the strategy intimately because he helped shape corporate messaging during his years inside Cigna before becoming one of the industry's most visible whistleblowers. Potter warned that focusing too narrowly on hospital pricing risks sanitizing the role insurers play in restricting care, designing burdensome authorization systems, and maximizing shareholder returns through administrative control over access.

His argument also holds substantial weight because insurers built extraordinarily profitable businesses around utilization management, claims denial infrastructure, and financial complexity. Publicly traded insurers consistently report strong margins even while patients face rising deductibles, narrower provider networks, and escalating administrative friction. Investors reward insurers for controlling medical loss ratios. Every delayed authorization, every disputed claim, and every layer of administrative review serves a measurable financial purpose inside that model.

The more important observation sits underneath both arguments. Hospitals and insurers do not merely oppose each other. They depend on each other economically. Their conflict operates inside a shared architecture that rewards complexity. The adversarial theater distracts from the fact that both industries benefit when pricing remains opaque, contracts remain confidential, and patients remain structurally incapable of functioning as informed consumers.

That complexity generates enormous economic value for institutions even while it imposes enormous cognitive and financial burdens on patients. Consider how many secondary industries exist purely because ordinary people cannot interpret healthcare billing systems. Revenue cycle management firms, coding consultants, utilization review vendors, third party billing companies, pharmacy benefit managers, prior authorization platforms, healthcare law practices, claims optimization firms, and patient advocacy services all monetize friction produced by systemic opacity. Entire sectors of the economy now exist to navigate the dysfunction of other sectors of the economy.

Patients experience the consequences directly. A family receives treatment at an in network hospital only to discover that the anesthesiology group contracted by the hospital operates outside the insurance network. A cancer patient undergoes imaging approved by one department only to receive a retroactive denial from another. A survivor receives an explanation of benefits statement that resembles encrypted tax code written by a sleep deprived accountant from 1987. Somewhere in the distance you can almost hear Max Headroom trying to explain deductible accumulation policies during a dial up modem connection.

The absurdity feels accidental when experienced individually. Viewed systematically, it reflects rational market behavior under current incentives.

Opacity protects negotiating leverage. Complexity justifies administrative overhead. Fragmentation weakens consumer bargaining power. Confusion delays political accountability because patients rarely know which institution actually caused the harm. By the time someone untangles the billing chain between hospital systems, insurers, pharmacy benefit managers, staffing contractors, and outsourced claims processors, exhaustion usually wins.

The healthcare industry often frames administrative complexity as an unavoidable byproduct of modern medicine. That explanation collapses under comparison with other sectors managing similarly sophisticated logistical systems. American consumers can track international package deliveries in real time, compare airline ticket prices across dozens of carriers instantly, and transfer money globally from a phone. Yet a patient undergoing chemotherapy still cannot reliably obtain an accurate estimate for treatment costs before care begins. That failure reflects incentive design, not technological limitation.

Hospitals defend high pricing by pointing to labor shortages, uncompensated care obligations, regulatory burdens, and declining reimbursement from public payers. Many of those concerns are legitimate. Healthcare labor costs increased substantially after the pandemic. Rural hospitals face severe financial pressure. Safety net institutions absorb enormous uncompensated care burdens. Academic medical centers support research infrastructure that private markets alone would not finance adequately.

Insurers defend utilization controls by pointing to overuse, fraud prevention, unnecessary procedures, and the need to contain premium growth. Some utilization management tools do prevent inappropriate care and help control costs. Healthcare spending in the United States already exceeds $4.5 trillion annually. Employers, taxpayers, and government programs cannot absorb unlimited inflation indefinitely.

Both industries can present defensible arguments because both industries operate inside structurally distorted incentives that reward institutional optimization over patient comprehension.

That distinction matters because most healthcare reform conversations collapse into moral theater instead of economic redesign. Public discourse often frames hospitals as greedy or insurers as evil, as though replacing individual executives would solve structural problems. Markets respond to incentives far more consistently than they respond to outrage. If policymakers want different outcomes, they must redesign the economic conditions producing current behavior.

Price transparency represents one obvious example. Genuine transparency threatens existing leverage structures because it exposes negotiated rate disparities, hidden markups, cross subsidization mechanisms, and administrative inefficiencies. Hospitals fear losing pricing power. Insurers fear losing control over negotiated discount narratives. Both industries comply minimally with transparency mandates while preserving as much informational asymmetry as possible.

Prior authorization offers another example. Insurers use authorization requirements to control spending and reduce unnecessary utilization. Hospitals respond by hiring large administrative staffs dedicated entirely to managing insurer paperwork. The resulting bureaucratic escalation consumes billions of dollars annually while shifting labor away from direct patient care. Nobody designed that system explicitly to harm patients. The incentive structure produced harm predictably anyway.

After 30 years inside cancer survivorship and healthcare advocacy, I no longer view most institutional behavior through a moral lens first. I view it through an incentive lens. Systems repeat behaviors that produce revenue stability, political protection, and market leverage. American healthcare consistently rewards opacity, fragmentation, and administrative escalation because those features preserve economic positioning for powerful stakeholders.

Patients absorb the cumulative consequences. Medical debt remains one of the leading contributors to personal bankruptcy in the United States. Delayed care increases downstream costs. Financial toxicity now functions as a measurable clinical burden in oncology because economic stress affects treatment adherence, mental health, housing stability, and long term survivorship outcomes. The system often treats those downstream consequences as unfortunate side effects instead of predictable outputs.

That institutional normalization of suffering partially motivated me to write We the Patients: Understanding, Navigating, and Surviving America's Healthcare Nightmare. I wanted to examine the healthcare system as an interconnected economic structure rather than a collection of isolated villains. Patients do not experience hospitals, insurers, pharmacy benefit managers, private equity firms, regulators, and employers separately. They experience the cumulative impact of all those forces simultaneously, usually while sick, frightened, and financially exposed.

Healthcare reform discussions frequently underestimate how strongly patient protection can align with economic efficiency when incentives realign appropriately. Transparent pricing reduces administrative waste. Simplified billing lowers collection costs. Earlier access to preventive and maintenance care reduces catastrophic downstream spending. Streamlined authorization systems improve labor productivity across both payer and provider organizations. Better aligned incentives could reduce friction while preserving sustainable margins for institutions that deliver genuine value.

Current incentives often reward the opposite behavior. The system compensates administrative navigation more reliably than prevention. It rewards market leverage more aggressively than simplicity. It monetizes fragmentation more effectively than coordination. Those dynamics will persist until regulators, employers, purchasers, and voters force alignment between institutional profitability and patient comprehensibility.

That challenge requires intellectual honesty from every side. Hospitals cannot continue presenting themselves solely as community guardians while aggressively consolidating regional markets and expanding facility fee structures. Insurers cannot continue presenting themselves as consumer protectors while deploying denial algorithms and opaque authorization systems that patients cannot realistically navigate alone. Policymakers cannot continue pretending that symbolic outrage substitutes for structural redesign.

The central issue no longer revolves around whether hospitals or insurers deserve more blame. The more consequential question asks whether the American healthcare economy can continue sustaining itself through administrative complexity without eventually collapsing public trust entirely. Systems that depend on consumer confusion eventually trigger political backlash, employer resistance, or market disruption once the burden exceeds tolerable limits.

Patients already reached that threshold years ago. Institutions simply continue debating whose turn it is to apologize while the invoice keeps growing.