What Happens If More Patients Appeal Insurance Denials?

The rational question sits in plain sight. What would happen if more patients appealed insurance denials.

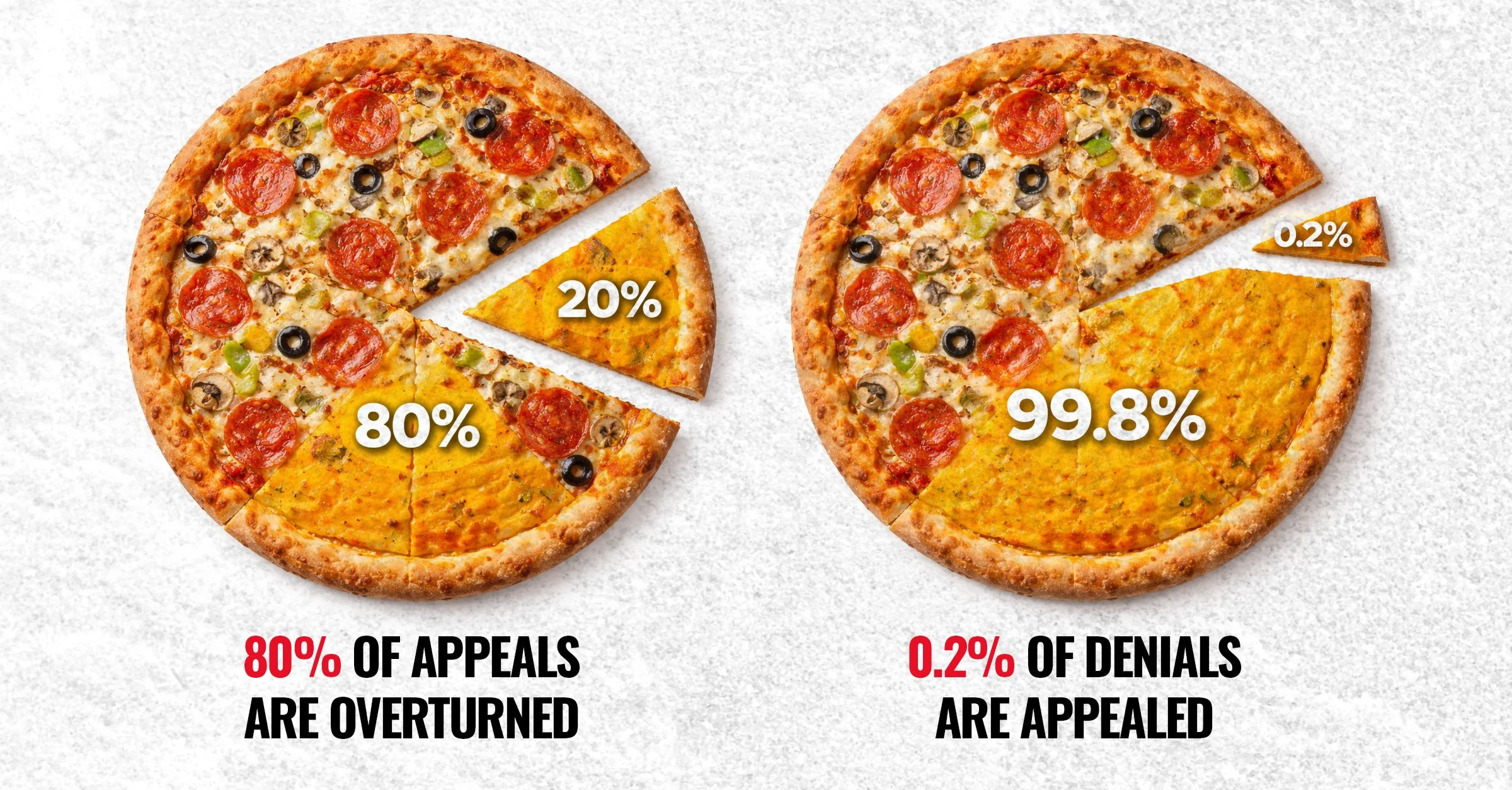

The data point looks almost trivial at first glance. About 80 percent of prior authorization appeals succeed. About 80 percent of prior authorization appeals succeed, according to the American Medical Association. About 0.2 percent of denials ever get appealed, based on KFF data from ACA marketplace plans.

The gap between those numbers deserves more attention than either number alone. If appeals rarely worked, low participation would reflect futility. If appeals happened often, high success rates would reflect a functioning safeguard. Neither condition exists. The system denies care at scale, most people do not challenge the decision, and when they do, they usually win.

That pattern signals design, not accident.

Start with the mechanics. Insurers manage cost through utilization control. Prior authorization and post service claim denials sit at the center of that control. Every denial delays or avoids spending. Every appeal consumes administrative time from physicians, staff, and patients. Every reversal restores access but still imposes friction.

From the insurer’s perspective, the optimal outcome balances three variables. Minimize payouts. Maintain regulatory compliance. Avoid reputational damage. A high denial rate paired with a low appeal rate achieves that balance. The system pays less without triggering widespread scrutiny because most denials never mature into disputes.

The success rate of appeals introduces a second layer. If 80 percent of appeals overturn denials, many initial denials lack durability under review. That does not automatically imply bad faith. It does suggest that first pass decisions operate under a different threshold than second pass decisions. The first pass screens volume. The second pass evaluates merit.

That distinction creates leverage.

Now consider what happens if appeal rates move even slightly. Take a simplified model. Assume 10 million denials in a given period. At a 0.2 percent appeal rate, 20,000 cases receive review. With an 80 percent overturn rate, 16,000 patients regain access. The system absorbs that cost as a manageable exception.

Increase appeals to 1 percent. That shifts 100,000 cases into review. With the same overturn rate, 80,000 patients receive care that would have remained denied. The incremental cost increases fivefold relative to the baseline.

Move to 5 percent. Now 500,000 cases undergo review. About 400,000 reversals follow. The cost exposure increases twenty five times relative to the baseline.

At 25 percent, the system processes 2.5 million appeals. About 2 million reversals follow. That level of engagement forces a structural response. Administrative systems strain. Medical review capacity expands. Denial criteria face continuous challenge.

These are not abstract shifts. They translate into real dollars.

Insurers price premiums based on expected medical loss ratios. Denials reduce paid claims and improve margins. If a larger share of denials convert into paid claims through appeals, medical loss ratios rise. Publicly traded insurers report those ratios quarterly. A sustained increase compresses margins and invites investor scrutiny.

Wall Street does not react to morality. It reacts to predictability. If appeal behavior becomes more common and less predictable, analysts adjust earnings models. That adjustment flows into valuations. Lower expected margins lead to lower multiples. Capital allocation decisions follow.

Insurance companies respond in kind. They can raise premiums, tighten initial authorization criteria, invest in more precise utilization management, or lobby for regulatory adjustments. Each response carries tradeoffs. Premium increases face employer resistance. Tighter criteria risk higher reversal rates on appeal. More precise management requires investment in data and personnel. Regulatory lobbying invites public attention.

The current equilibrium avoids those tradeoffs because the volume of appeals stays negligible.

Employers sit in the middle of this system. Many large employers self fund health plans and contract insurers for administration. They care about total cost of care, employee productivity, and retention. If more employees appeal denials and succeed, employers see higher claims costs. They also see fewer delays in care, fewer complications from untreated conditions, and potentially lower downstream costs.

That creates a tension between short term expense and long term efficiency.

Delayed care often costs more. A denied diagnostic test can lead to a missed diagnosis. A denied therapy can lead to disease progression. When those cases re enter the system, they require more intensive and more expensive interventions. Appeals that restore timely care can reduce those downstream costs. The financial benefit does not always accrue in the same fiscal period. It still exists.

From a macroeconomic perspective, increased access to medically necessary care supports workforce participation. Healthier individuals work more consistently, contribute more productively, and rely less on disability or emergency services. Those effects accumulate across millions of people.

Now examine the operational reality. Why do so few people appeal.

The process demands time, literacy, and persistence. Patients must interpret denial letters, gather documentation, coordinate with clinicians, and navigate insurer specific procedures. Many patients face illness, financial stress, and administrative fatigue at the same time. The system imposes friction at each step.

Clinicians face their own constraints. Appeals require documentation, peer to peer calls, and staff coordination. Many practices lack dedicated personnel to manage denials. Time spent on appeals competes with time spent on patient care. Reimbursement rarely covers that administrative work.

These frictions function as a filter. They reduce the number of appeals without requiring explicit restrictions. The system does not need to block appeals. It needs to make them costly enough in time and effort that most people opt out.

That design aligns with the economic incentives described earlier.

Consider the counterfactual. A system where 25 percent of denials receive appeals requires different infrastructure. Insurers would need larger clinical review teams. Standardization of criteria would become more important to reduce reversal rates. Automation might handle initial screening, but human review would expand for contested cases.

Providers would need support staff dedicated to utilization management. Some already do. That model would become more common. Third party services that assist with appeals would grow. Technology platforms that streamline documentation and submission would gain traction.

Regulators would likely respond as well. Higher appeal volumes would generate more data on denial patterns. That data could inform policy changes around transparency, timeliness, and criteria. External review processes could expand.

The system would become more contested and more visible.

Visibility changes behavior.

When denial practices operate in relative obscurity, they evolve to optimize internal metrics. When those practices face frequent challenge and public data, they evolve to withstand scrutiny. That does not eliminate denials. It changes their composition.

Some institutional defenses deserve consideration. Insurers argue that utilization management prevents unnecessary or low value care. Evidence supports the existence of overuse in certain areas of medicine. Any system that pays for every requested service without review would increase costs and expose patients to unnecessary interventions.

That argument holds in principle. It loses force when high reversal rates indicate that many denied services meet medical necessity upon review. If initial denials regularly fail under scrutiny, the system misclassifies necessary care as unnecessary at scale.

A well aligned system would minimize both overuse and underuse. It would approve necessary care efficiently and flag questionable care with clear rationale. It would resolve disputes quickly with minimal burden on patients and clinicians.

The current system achieves cost control in part by shifting the burden of proof onto patients and providers. It relies on low engagement with the appeals process to sustain that model.

The economic question then becomes straightforward. What happens when engagement increases.

At 1 percent appeal rates, the system absorbs higher costs but remains stable. At 5 percent, the pressure becomes noticeable in financial reports and operational workflows. At 25 percent, the system must adapt structurally. It cannot rely on passive acceptance of denials.

Adaptation could take several forms. Insurers could refine initial decision making to reduce the number of denials that would be overturned. That would lower administrative waste and improve patient experience. They could invest in clearer communication of criteria to providers. They could shorten timelines for decisions and appeals to reduce delays.

Providers could integrate appeals into care pathways rather than treat them as exceptions. Technology could reduce administrative burden. Patients could access clearer guidance on how to respond to denials.

Each of these changes aligns patient protection with economic efficiency. Fewer incorrect denials reduce administrative churn. Faster access to necessary care reduces complications. Clearer criteria reduce disputes.

The alternative path involves shifting costs through higher premiums or narrower networks without addressing underlying inefficiencies. That path preserves margins in the short term and erodes trust over time.

Trust carries economic value. Employers choose plans based on cost and employee experience. Patients choose providers and insurers based on perceived reliability. Regulators respond to public pressure when trust declines.

A system that denies care and relies on low appeal rates to sustain margins risks long term instability. A system that aligns incentives to approve necessary care efficiently and contest questionable care transparently supports both financial performance and public confidence.

The difference hinges on engagement.

Patients do not need to become policy experts to change this dynamic. Small increases in appeal rates shift the equilibrium. Moving from 0.2 percent to 1 percent multiplies the number of contested decisions by five. That change alone introduces more data, more scrutiny, and more cost exposure.

From there, feedback loops develop. As more people appeal and succeed, awareness grows. As awareness grows, behavior changes. As behavior changes, institutions respond.

This dynamic resembles other systems where participation drives accountability. When very few people vote, outcomes reflect a narrow slice of the population. When more people vote, outcomes shift. The same principle applies here, with different stakes and mechanisms.

The healthcare system will continue to behave rationally within its incentive structure. It will optimize for cost control, compliance, and reputation. If low appeal rates remain the norm, high denial rates with high reversal potential can persist without disruption.

If appeal rates increase, the cost of incorrect denials rises. The system must then decide whether to improve initial accuracy, absorb higher costs, or redesign processes.

That decision does not require moral framing. It follows directly from incentives.

The country does not need a wholesale reinvention of insurance to see change. It needs a recalibration of participation in the mechanisms that already exist. Appeals represent one of those mechanisms.

Increase their use, and the system adjusts. Leave them underused, and the current equilibrium holds.

The consequences of each path will show up in financial statements, regulatory agendas, clinical workflows, and patient outcomes. The choice of path does not belong to a single institution. It emerges from millions of individual decisions to accept or challenge a denial.

Right now, almost everyone accepts.

That behavior keeps the system stable.

Changing that behavior, even slightly, changes the system.